Using Enterprise Budgets to Compute Crop Breakeven Prices

Enterprise budgets provide an estimate of potential revenue, expenses, and earnings or losses for a specific enterprise. Enterprise budgets are often one of the building blocks to creating a whole-farm plan. They are also extremely useful in computing breakeven prices. This article uses a cash crop farm in Indiana to illustrate the components of an enterprise budget and to compute breakeven prices for corn and soybeans. The format of the enterprise budget presented below closely follows that of the Purdue Crop Cost and Return Guide (here). The Illinois crop budgets (here) use similar cost items, but are laid out differently. Both budgets use all costs, thus breakeven prices could be computed using either budget layout.

Most enterprise budgets use economic costs rather than cash costs. This means that, in addition to cash costs and depreciation, opportunity costs are included. An opportunity cost represents the income that could have been earned if an input was sold or rented to someone else. Opportunity costs for unpaid family and operator labor, owned machinery, and owned land need to be included in an enterprise budget. Because opportunity costs are included in an enterprise budget, the bottom line figure (i.e., earnings or losses) represents an economic profit or loss. Over a long period of time, due to the fact that all inputs (cash items, depreciation, and opportunity costs) are being paid the market rate, economic profit is zero. If economic profit is positive, input prices will be bid up, similar to what happened to cash rents during the last decade, and economic profit will migrate towards zero. Conversely, if economic profit is negative, input prices will decline, and economic profit will head towards zero or breakeven.

Rotation Corn Budget

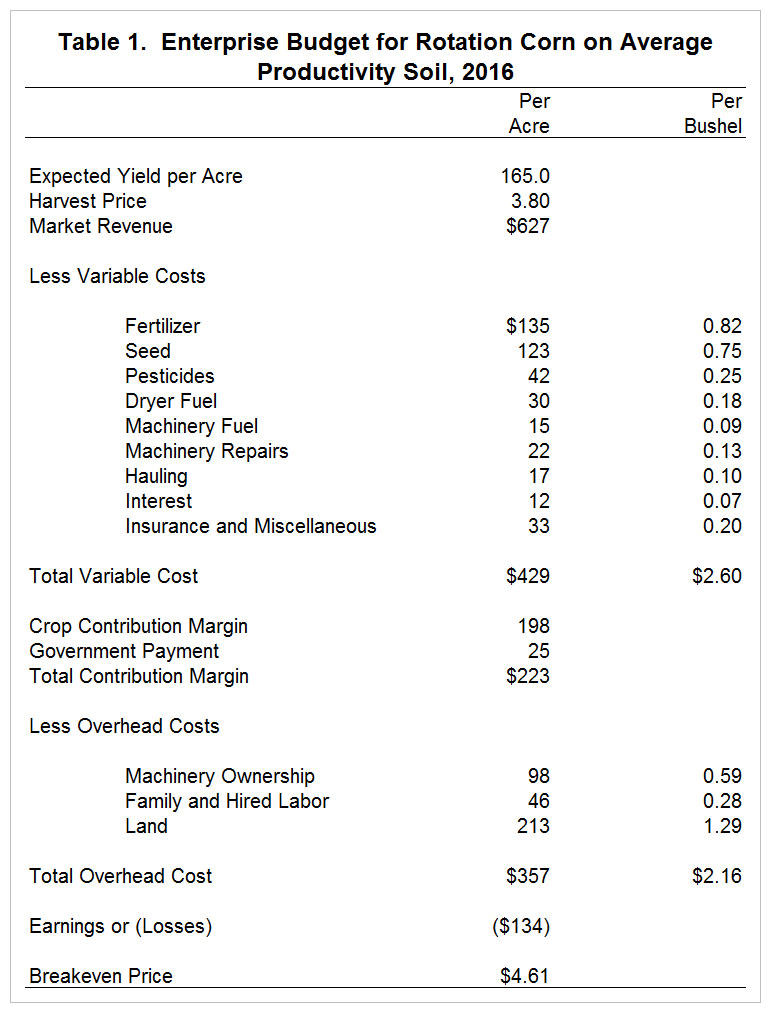

Table 1 presents an enterprise budget for rotation corn on average productivity soil in Indiana for 2016. Trend yield multiplied by the expected harvest price results in a market revenue of $627 per acre. Costs are presented on a per-acre and a per-bushel basis. Both of these figures can be useful when examining a particular cost item. Per-acre costs are typically easier to benchmark (with other farms or using historical information for the same farm) while per-bushel costs are extremely useful in examining the impact on a particular cost item when making a change that impacts yield per acre. Total variable cost is $429 per acre ($2.60 per bushel). Subtracting total variable cost from market revenue and adding government payments yields an expected total contribution margin of $223 per acre. For the enterprise to breakeven, the total contribution margin needs to be at least as large as total overhead cost. For 2016, the total contribution margin for rotation corn is expected to be substantially smaller than total overhead costs, resulting in a loss per acre of $134. Breakeven price is computed by adding total variable cost to total overhead cost, subtracting government payments, and dividing the result by expected yield per acre. Breakeven price for corn is estimated to be $4.61 per bushel.

The breakeven price reported in table 1 is sensitive to changes in yields, prices, and cost estimates. For example, a reduction in land cost of 10% results in a breakeven price of $4.48 or a 2.8% reduction in breakeven price. As another example, the 2015 budget estimated fertilizer cost at $147 per acre. The estimated decline in fertilizer cost of $12 per acre results in a reduction in fertilizer cost per bushel of $0.07 per bushel. It is important to note that the same fertilization program was used for both the 2015 and 2016 budgets.

Rotation Soybean Budget

Table 2 presents an enterprise budget for rotation soybeans on average productivity soil for 2016. Trend yield multiplied by the expected harvest price results in a market revenue of $420 per acre. Variable cost is $216 per acre or $4.32 per bushel. After subtracting total variable cost from market revenue and adding government payments, total contribution margin per acre is $229. Though slightly larger than the expected contribution margin for corn, the contribution margin for soybeans is still not large enough to fully cover overhead costs. Expected loss per acre is $128. Breakeven price for soybeans is estimated to be $10.96 per bushel.

The breakeven price for soybeans reported in table 2 is sensitive to changes in yields, prices, and cost estimates. For soybeans, a 10% reduction in cash rent results in a 3.9% decrease in breakeven price (a drop from $10.96 to $10.53). Notice that the percentage drop in the breakeven price for soybeans resulting from a 10% decline in cash rent is higher than the corresponding decline in the breakeven price for corn. This is due to the fact that overhead costs on a per-bushel basis are relatively more important for soybeans than corn. Total overhead cost as a percentage of total cost for soybeans is 62%. In contrast, for corn this percentage is 45%.

Final Comments

It is important to note that opportunity costs for unpaid family and operator labor, owned machinery, and owned land are included in tables 1 and 2. If we want to compare revenue, costs, and earnings between farms; it is important to include these opportunity costs. Also, if we want to gauge the return to operator time and owned assets, these opportunity costs need to be included in enterprise budgets. The negative earnings or losses per acre depicted in tables 1 and 2 suggest that owned assets are not receiving market rates of return.

As a final note, enterprise budgets can be used to make cropping decisions for the upcoming year. Though both corn and soybeans show losses in tables 1 and 2, the loss per acre for soybeans is less than the loss per acre for corn. The contribution margin for both crops is positive. In the short-run, a farm should continue to produce if it is covering variables costs (i.e., the total contribution margin is positive). In the long-run, all costs (variable and overhead costs) need to be covered. The higher contribution margin for soybeans does not imply that the farm should produce all soybeans. It does, however, imply that the farm should consider producing both corn and soybeans, rather than focusing on corn, which some farms have done since the start of ethanol boom in 2007.

This article used a cash crop farm in Indiana to illustrate the components of an enterprise budget and to compute breakeven prices for corn and soybeans. Components of the enterprise budgets for corn and soybeans included gross revenue, variable costs, contribution margin, overhead costs, and earnings or losses. Costs should be presented on a per-acre and a per-bushel basis. Using the information in this article, breakeven prices for corn and soybeans for 2016 were projected to be $4.61 and $10.96, respectively.

References

Purdue Agriculture Center for Commercial Agriculture. Purdue Crop Budget Archive. https://ag.purdue.edu/commercialag/Pages/Resources/Management-Strategy/Crop-Economics/Crop-Budget-Archive.aspx

Schnitkey, G. "Crop Budgets, Illinois, 2016." Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, September 2015.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.