Assessing the Capital Adequacy of U.S. Commercial Banks Participating in Agricultural Lending

In this article, we conclude our series on U.S. Commercial Bank participation in agricultural lending. In our previous article (farmdoc daily, June 20, 2024), we examined the differences in profitability between agricultural and non-agricultural commercial banks. As of the fourth quarter of 2023, on average, commercial banks specializing in agricultural lending reported higher Returns on Average Assets and were more cost-efficient than non-agricultural banks. However, non-agricultural banks reported higher average Net Interest Margins. Within both lending specializations, the average Net Interest Margin and Efficiency Ratio decreased as the bank asset size increased. We now extend this analysis by examining the differences in capital adequacy between agricultural and non-agricultural commercial banks. We limit our analysis to Federal Deposit Insurance Corporation (FDIC)-insured commercial banks that have outstanding farm real estate and farm operating loans on their balance sheets as of the fourth quarter of 2023. Two lending specializations are defined. Commercial banks whose sum of farm real estate and farm operating loans exceeds 25% of their net loans and leases are defined as agricultural banks, while all others are defined as non-agricultural banks. 1,022 commercial banks were categorized as agricultural banks, while 2,518 were categorized as non-agricultural banks.

A bank’s capital serves as a buffer against unforeseen losses and asset devaluations that could potentially lead to bank failure. Given that banks typically maintain relatively low levels of capital compared to the size of their balance sheets, careful monitoring of their financial condition by regulators and examiners is essential to safeguard the stability of the banking system. Capital adequacy is one of the crucial components of bank financial health that regulators monitor. Its evaluation considers both qualitative and quantitative factors. Quantitative factors are primarily represented by minimum capital requirements established by regulatory agencies. These requirements are usually expressed as ratios comparing a bank’s capital to its risk-weighted or total assets, providing a standardized measure of its financial strength relative to its risk exposure. Banks exposed to higher levels of risk are expected to maintain capital levels above the regulatory minimums. The two categories of capital are Tier 1 capital and Tier 2 capital. Tier 1 capital is the core capital of a bank, while Tier 2 capital is supplementary capital and is less secure than Tier 1 capital.[1] In this article, we will evaluate the Tier 1 risk-based capital ratio and the total risk-based capital ratio of commercial banks participating in agricultural lending. For both capital adequacy measures, a higher ratio indicates that a bank is better positioned to withstand losses and less likely to experience insolvency.

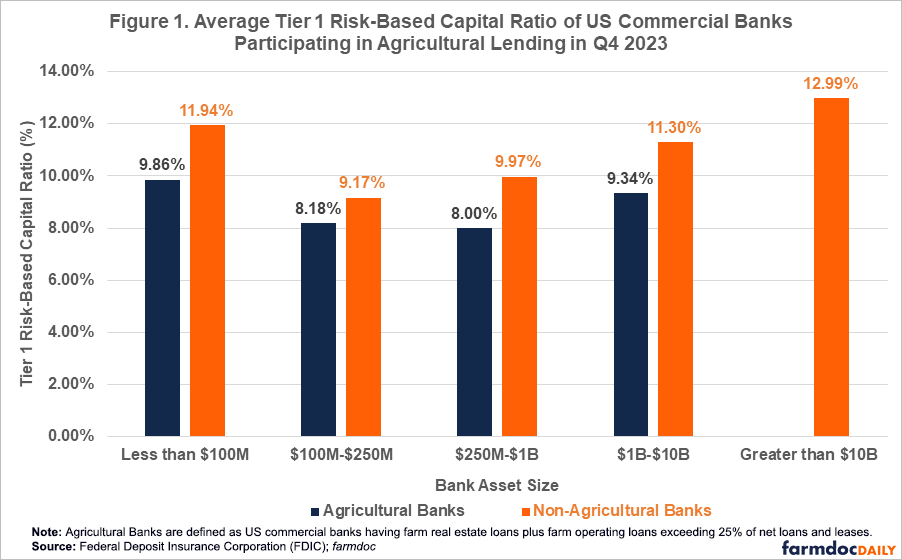

The Tier 1 risk-based capital ratio is the ratio of a bank’s tier 1 capital to its risk-weighted assets. According to the FDIC, all FDIC-supervised commercial banks are required to maintain a minimum Tier 1 risk-based capital ratio of 6 percent (FDIC, 2022). Figure 1 shows that, on average, both agricultural and non-agricultural banks reporting in the fourth quarter of 2023 met this minimum requirement. However, agricultural banks consistently reported lower Tier 1 risk-based capital ratios compared to non-agricultural banks across all asset size categories. Among agricultural banks, those with assets between $250 million and $1 billion had the lowest average ratio at 8.00%, while those with assets less than $100 million had the highest average ratio at 9.86%. For non-agricultural banks, those with assets exceeding $10 billion had the highest average Tier 1 risk-based capital ratio at 12.99%, followed by banks with assets less than $100 million at 11.94%. Non-agricultural banks with assets of $100 million to $250 million had the lowest average ratio at 9.17%.

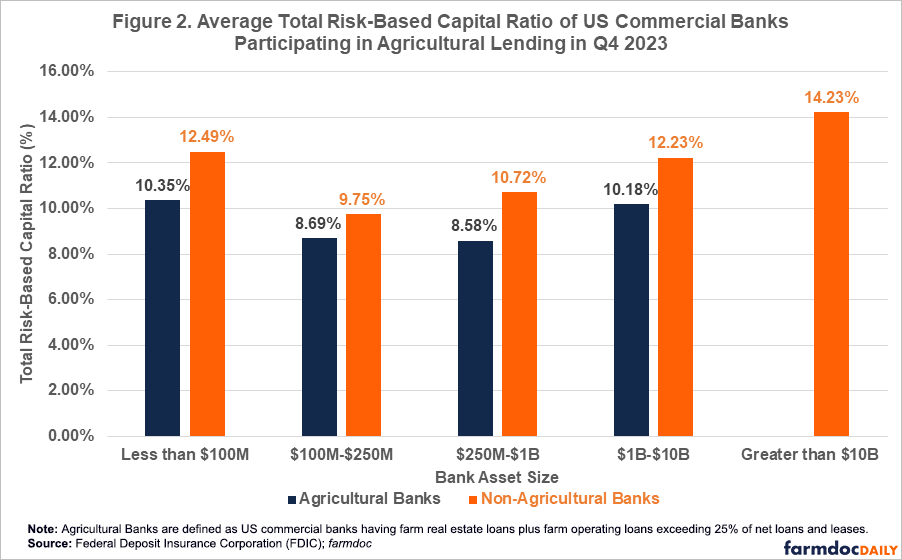

The total risk-based capital ratio is the ratio of a bank’s total (Tier 1 + Tier 2) capital to its risk-weighted assets. According to the FDIC, all FDIC-supervised commercial banks are required to maintain a minimum total risk-based capital ratio of 8 percent (FDIC, 2022). Figure 2 illustrates that, on average, the minimum requirement was met by both agricultural and non-agricultural banks reporting in the fourth quarter of 2023. However, agricultural banks consistently reported lower total risk-based capital ratios compared to non-agricultural banks across all asset size categories. Furthermore, on average, agricultural banks with an asset size of $100 million to $250 million and $250 million to $1billion were only slightly above the minimum requirement, at 8.69% and 8.58%, respectively. Among agricultural banks, those with assets of less than $100 million had the highest total risk-based capital ratio at 10.35%, followed by those with an asset size of $1 billion to $10 billion at 10.18%. For non-agricultural banks, those with an asset size greater than $10 billion had the highest total risk-based capital ratio at 14.23%, followed by those with assets less than $100 million at 12.49%. Non-agricultural banks with assets of $100 million to $250 million had the lowest ratio at 9.75%.

Conclusion

In conclusion, our analysis of Tier 1 and total risk-based capital ratios reported in the fourth quarter of 2023 reveals important insights into the financial health of agricultural and non-agricultural commercial banks. While both types of banks met the minimum regulatory requirements, agricultural banks consistently demonstrated lower capital ratios across all comparable asset size categories. In 2023, we witnessed three of the four largest bank failures in US history: First Republic Bank, Silicon Valley Bank, and Signature Bank. These high-profile collapses serve as a stark reminder of the importance of maintaining adequate capital ratios and implementing effective risk management practices. In the case of First Republic, its failure was a result of its reliance on uninsured deposits, which accounted for 64% of its assets, and a failure to sufficiently mitigate interest rate risk (FDIC’s Supervision of First Republic Bank, 2023). Despite these high-profile failures, the banking industry has demonstrated resilience. According to the FDIC, the number of banks on the FDIC’s Problem Bank List increased from 52 in the fourth quarter of 2023 to 63 in the first quarter of 2024 (FDIC Quarterly Banking Profile, 2024Q1). However, they only represent 1.4% of total banks, indicating that the vast majority of banks remain stable.

Note

[1] Tier 1 capital consists of common stock, retained earnings, and accumulated other comprehensive income. Tier 2 capital consists of loan-loss reserves, subordinated debt, revaluation reserves, hybrid instruments, and undisclosed reserves.

References

Federal Deposit Insurance Corporation. (2024). FDIC Quarterly Banking Profile: First Quarter 2024. Retrieved from https://www.fdic.gov/news/speeches/fdic-quarterly-banking-profile-first-quarter-2024

Federal Deposit Insurance Corporation. (2023). FDIC’s Supervision of First Republic Bank. https://www.fdic.gov/sites/default/files/2024-03/pr23073a.pdf

Federal Deposit Insurance Corporation. (2022). Capital. Risk Management Manual of Examination Policies (Section 2.1). https://www.fdic.gov/resources/supervision-and-examinations/examination-policies-manual/section2-1.pdf

Mashange, G. "Assessing the Profitability of U.S. Commercial Banks Participating in Agricultural Lending." farmdoc daily (14):115, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, June 20, 2024.

Disclaimer: We request all readers, electronic media and others follow our citation guidelines when re-posting articles from farmdoc daily. Guidelines are available here. The farmdoc daily website falls under University of Illinois copyright and intellectual property rights. For a detailed statement, please see the University of Illinois Copyright Information and Policies here.